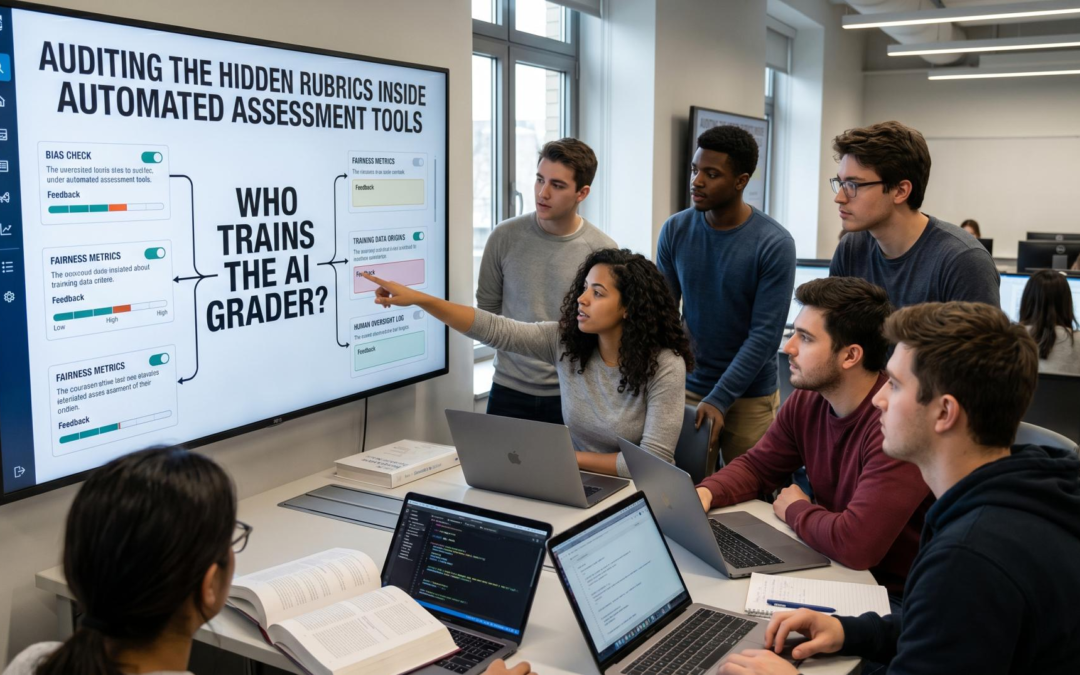

WHO TRAINS THE AI GRADER? AUDITING THE HIDDEN RUBRICS INSIDE AUTOMATED ASSESSMENT TOOLS

Automated grading tools are marketed on consistency and speed, and on both counts they often deliver. What they rarely deliver is transparency about what they’re actually rewarding, and that gap is becoming a real institutional liability as these tools move from grading multiple-choice quizzes into evaluating open-ended student writing and reasoning.

The Black Box of Automated Grading

Most institutions adopting AI grading tools know remarkably little about how the underlying model arrives at a score. Vendors describe their products in terms of outcomes, alignment with human grader scores, faster turnaround, reduced grading fatigue, but rarely disclose the actual rubric the model has learned to apply. That rubric isn’t written down anywhere a teacher can review it. It’s encoded implicitly in the patterns the model picked up during training, which means it can reward things no one ever intended it to reward.

What Rubrics Are Actually Encoded

Research on automated essay scoring has repeatedly found that these systems can latch onto superficial proxies, sentence length, vocabulary sophistication, even punctuation patterns, that correlate with quality in the training data without actually measuring the reasoning or argument quality teachers care about. A model trained on a set of human-graded essays will absorb whatever biases existed in that grading, including unconscious preferences for certain writing styles or familiar phrasing patterns that have nothing to do with the rigor of the underlying thinking. The institution adopting the tool inherits those biases without ever seeing them named.

The Case for Audits

This is not a new problem in principle. Algorithmic auditing is a mature practice in domains like lending and hiring, where the consequences of biased automated decisions are well understood and increasingly regulated. Education has been slower to apply the same scrutiny to assessment tools, partly because the stakes of a single grading decision feel smaller than a loan denial. But aggregated across an entire institution and an entire student population, a systematically biased grading rubric has the same kind of structural impact, just distributed more quietly.

Building an Audit Framework

Institutions don’t need to build sophisticated technical auditing capacity from scratch to start addressing this. A practical starting point is sample testing, periodically having human graders score a representative sample of the same student work the AI tool graded, and comparing not just the scores but the apparent reasoning behind discrepancies. Building a structured teacher review loop, where flagged or borderline AI scores get routed to a human grader before being finalized, catches the worst failures without abandoning the efficiency gains entirely. And procurement teams should be treating vendor transparency about training data and known failure modes as a contractual requirement, not a nice-to-have. A vendor unwilling to disclose what their model has been shown to over-reward or under-reward is asking institutions to adopt a rubric they’re not allowed to see.

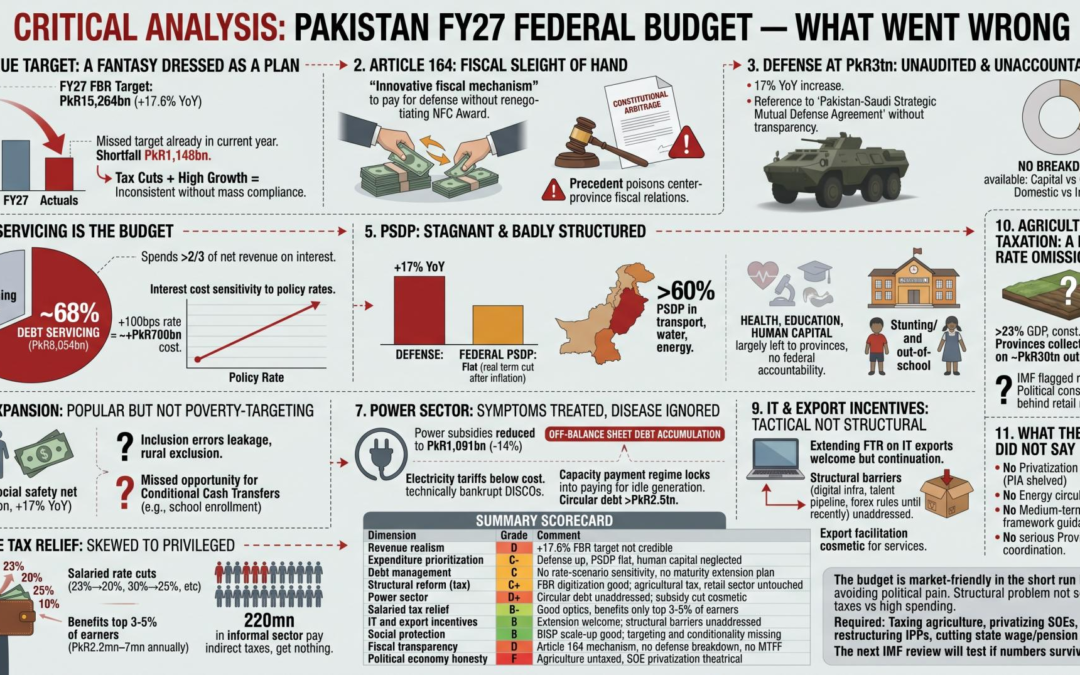

This is a structural critique, not a political one. The budget has genuine positives, but several decisions are either analytically weak, fiscally reckless, internally contradictory, or represent missed reform opportunities that Pakistan may not get again for years.

The Revenue Target Is a Fantasy Dressed as a Plan

The FBR target of PkR15,264bn (+17.6% YoY) is the budget’s most dangerous number.

The current year’s revised estimate already missed the original PkR14,131bn target, coming in at PkR12,983bn — a shortfall of PkR1,148bn. Pakistan’s FBR has never delivered 17.6% growth on a realistic base in a single year through genuine broadening of the tax net. Every time they’ve come close, it was driven by inflation (more rupees chasing same goods) or one-off measures, not structural reform.

Now they are simultaneously cutting super tax, slashing WHT on property, reducing IT and export taxes, and abolishing multiple levies — all of which reduce the tax take — while expecting 17.6% revenue growth. These two things cannot coexist without either massive new compliance enforcement (which has never materialized in Pakistan’s history) or a mid-year mini-budget.

What should have been done: Set a realistic 10–12% growth target and front-load the structural reforms to broaden the base — agricultural income tax (a constitutional provincial subject but politically avoidable), taxing the retail and wholesale trade sector properly (not a flat 1% regime that formalizes under-declaration), and moving the documented-to-undocumented economy ratio from the current ~40% toward 60% over three years with binding milestones. The FBR Reform section (National Faceless Centre, double-blind audit) is genuinely good — but it’s a medium-term intervention being sold as an FY27 revenue contributor, which it is not.

The Article 164 Mechanism Is Fiscal Sleight of Hand

The budget introduces a “cooperative federalism” mechanism under Article 164 — incremental FBR collections between PkR13,350bn and PkR15,264bn flow back to the Federation as strategic grants to finance defense. The document calls it “an innovative fiscal mechanism.”

What it actually is: a method to pay for a PkR3tn defense budget without formally renegotiating the 7th NFC Award, so provincial shares remain nominally intact while the Federation reroutes the incremental collection. This is not fiscal innovation — it is constitutional arbitrage. It sets a precedent that the NFC Award is circumventable by executive design, which will poison center-province fiscal relations for years. Khyber Pakhtunkhwa and Sindh in particular have strong incentives to challenge this legally, and they should.

More importantly, the mechanism only works if FBR collects the incremental PkR1,914bn (from PkR13,350bn to PkR15,264bn). Given the above analysis on revenue targets, this incremental amount is almost certainly not going to be collected, meaning the Federation either borrows to fund defense or cuts civilian spending mid-year.

What should have been done: A transparent renegotiation of the NFC Award to reflect contemporary expenditure realities — particularly on defense and federal development — rather than engineering workarounds that undermine the constitutional architecture.

Defense at PkR3tn Is Unaudited and Unaccountable

Defense spending rose 17% YoY to PkR3tn, justified by “post-Operation Bunyan-ul-Marsous realities and the Pakistan-Saudi Strategic Mutual Defense Agreement.” There is no breakdown of this PkR3tn in the public budget documents. Capital vs. current. Personnel vs. procurement. Domestic vs. import-dependent.

For context, defense at PkR3tn now represents approximately 2.09% of nominal GDP (PkR143.6tn) and is larger than the entire Federal PSDP (PkR1tn). Pakistan spends more on military than on development. This is not abnormal by South Asian standards, but it is unsustainable at this deficit level.

The more pressing issue: the Pakistan-Saudi Strategic Mutual Defense Agreement is referenced as fiscal justification for a 17% surge in defense spending, but the terms of this agreement have not been placed before parliament. Tying permanent expenditure increases to undisclosed bilateral commitments is a governance failure.

What should have been done: Even a high-level defense budget breakdown (capital vs. recurrent; percentage domestically produced vs. imported) would allow economists and parliament to assess the import-bill impact and the domestic multiplier effect. Pakistan’s defense imports consume scarce foreign exchange and generate minimal domestic value-add. Without visibility, we cannot optimize.

Debt Servicing Is the Budget — Everything Else Is Residual

Debt servicing at PkR8,054bn represents 43% of total expenditure and 68% of net revenue receipts. Pakistan is spending more than two-thirds of every rupee it collects in net revenues on interest payments alone. This ratio has improved from its FY25 peak (where debt servicing briefly exceeded net revenue receipts entirely), but it remains structurally crippling.

The budget treats the decline in debt servicing as a success story — and technically, the drop from PkR8,206bn (budgeted FY26) to PkR8,054bn (FY27 budget) is progress driven by falling rates. But the FY27 budget simultaneously assumes 11.5% policy rate (post the April hike) with possible further tightening in June, which means T-Bill rollovers and PIB auctions through FY27 will be priced at rates higher than assumed when this debt-servicing estimate was computed.

If the June 15 MPC delivers another 50–100bps hike (which 49% of surveyed analysts expect), the PkR8,054bn estimate is immediately undercooked. Every 100bps increase on a ~PkR70tn domestic debt stock adds roughly PkR700bn in annual interest cost — the entire BISP budget wiped out in one rate decision.

What should have been done: The budget needed a sensitivity table showing debt servicing under 11.5%, 12%, and 12.5% policy rate scenarios. It also needed an aggressive domestic debt maturity extension program — locking in current rates by issuing long-duration Sukuks and PIBs before any further hikes — rather than continuing to rely on short-duration T-Bill rollovers that amplify rate exposure.

The PSDP Is Stagnant and Badly Structured

Federal PSDP is maintained at PkR1,000bn — same as FY26’s budgeted figure. At face value, this looks like continuity. In real terms, it is a cut (inflation of 8.2% implies PkR918bn in real PkR26 terms). Against a PkR18.8tn expenditure budget, the development allocation is 5.3% of total spending.

The structural problem: over 60% of PSDP is in transport, water, and energy. These are legitimate priority sectors, but this concentration means health, education, and human capital development — the actual drivers of long-run productivity — are largely left to provinces through the NFC transfer, with no federal accountability mechanism for outcomes.

Pakistan’s human development indicators are catastrophic for a lower-middle income country. ASER Pakistan consistently shows over 22 million out-of-school children. Stunting affects ~40% of children under 5. These are not solvable through transport infrastructure alone. A budget that raises defense by 17% and holds PSDP flat is implicitly choosing short-run security over long-run productivity.

The other structural flaw: PSDP execution has averaged roughly 70–80% of allocation for years. Budgeting PkR1,000bn when you know PkR700–750bn will actually flow is poor public financial management. Either budget what you can execute, or fix the execution machine — the budget does neither.

What should have been done: Reduce PSDP headline to PkR800bn with a realistic execution plan, allocate 20–25% to human capital (nutrition, teacher training, primary health), and link remaining disbursements to measurable deliverables rather than phased allocations that stall in bureaucracy.

BISP Expansion Is Politically Popular but Not Poverty-Targeting

BISP allocation at PkR838bn (+17% YoY) is the largest social safety net in Pakistan’s history, and this is a genuine achievement. However, several structural critiques apply:

First, 17% growth in BISP spending while real GDP grows at 4% means BISP is growing 4x faster than the economy. This is only sustainable if it is being financed by genuine revenue growth — which we established above is unlikely.

Second, the BISP beneficiary database has well-documented inclusion errors. Multiple audits and BISP’s own data show significant leakage to non-poor households and exclusion of genuinely poor households, particularly in rural Balochistan and FATA. Throwing 17% more money into a targeting system that hasn’t been rigorously re-validated is wasteful.

Third, BISP is unconditional cash. There is strong international evidence for conditional cash transfers — tying payments to school enrollment, vaccination, or maternal health checkups — generating better development outcomes per rupee spent. Pakistan’s own evidence base from pilot programs supports this. The budget missed an opportunity to shift BISP toward conditionality at scale.

Power Sector: Symptoms Treated, Disease Ignored

Power subsidies are reduced to PkR1,091bn (-14% YoY). This looks like fiscal discipline. It isn’t — it’s a reduction in one line item while the circular debt stock continues accumulating off-balance-sheet in the power sector’s borrowings from commercial banks.

The structural problem is that electricity tariffs remain well below cost-recovery for residential consumers, the distribution companies (DISCOs) are technically bankrupt loss-making SOEs hemorrhaging PkR400–600bn per year in T&D losses and theft, and the capacity payment regime (the result of take-or-pay IPP contracts signed in 2015 and 2021) locks Pakistan into paying for idle generation capacity regardless of demand.

Nothing in the FY27 budget addresses the root cause: either restructure the IPP contracts (which the government started doing in FY25 but quietly stalled), aggressively privatize/corporatize DISCOs with a hard political mandate, or move to cost-reflective tariffs with targeted subsidy for the lowest consumption bracket only.

The budget’s power sector answer is: reduce the subsidy line item and hope the problem migrates off the headline budget. The circular debt stock has already crossed PkR2.5tn. This is a crisis deferred, not resolved.

The Income Tax Relief Is Skewed to the Already-Privileged

The salaried class tax relief — rate reductions from 23%?20%, 30%?25%, 35%?29% and 35%?32% for incomes between PkR2.2mn and PkR7mn annually — is being presented as middle-class relief. These are actually incomes between roughly $7,800 and $25,000 per year at current exchange rates. The people earning PkR2.2mn–7mn annually are in the top 3–5% of Pakistan’s income distribution.

Pakistan’s total documented salaried taxpayer base is approximately 2.5–3 million people in a country of 257 million. The budget reduces the tax burden on these 2.5 million people while doing essentially nothing for the 220 million in the informal sector who pay indirect taxes (GST, FED) on every item they buy but have no formal income tax obligation because they are undocumented.

The abolition of the income surcharge is the same story: this was charged only on salaried incomes above PkR10mn — i.e., the top fraction of the top 5%. Abolishing it costs the government revenue and delivers a benefit entirely to the richest documented earners. Framing this as salaried class relief is a messaging choice, not an economic characterization.

What should have been done: the marginal rate cuts should have focused on the PkR600,000–PkR2.2mn annual income bracket (annual salary of PkR50,000–183,000/month), which represents the genuinely vulnerable lower-middle documented class. The upper bracket already benefits from cost-of-living perks, car allowances, medical, and bonus structures that are effectively tax-free.

The IT and Export Incentives Are Tactical, Not Structural

Extending the 0.25% FTR on IT exports to June 2029 is welcome, but it is a continuation of a regime due to expire — not an expansion. Pakistan’s IT exports were approximately $3.2bn in FY25, against India’s $254bn and Egypt’s $6bn (a country with a smaller tech talent base). The gap is not primarily because of tax rates. It is because of regulatory friction (forex repatriation rules until recently), inadequate digital infrastructure outside Karachi/Lahore/Islamabad, visa difficulty for foreign clients visiting Pakistan, and the talent pipeline bottleneck.

None of these structural barriers are addressed in the budget. The export facilitation measures (EFS markup at 4.5%, 9?18 month extension) are useful for manufacturing exporters but cosmetic for services exporters.

The reduction in WHT on international card transactions from 5% to 0.5% is overdue and genuinely beneficial for freelancers and IT firms, and this is one of the budget’s cleaner wins. However, even this measure was only necessitated by the fact that Pakistan drove significant dollar transactions underground through an indefensible 5% levy in the first place.

Agricultural Taxation: A Deliberate Omission

Agriculture contributes roughly 23% of GDP and is constitutionally taxed at the provincial level. Provinces consistently fail to collect meaningful agricultural income tax — the total collected across all four provinces is typically under PkR10bn annually on a sector generating PkR30+ trillion in output. This is the single largest source of tax expenditure in Pakistan’s fiscal system, and it is entirely absent from the FY27 federal budget.

The IMF has flagged agricultural income taxation repeatedly. The FBR Reform section is eloquent about digital audit trails and faceless tax centres. None of it touches the feudal land-owning class that structurally dominates parliament and has blocked this reform for 75 years. A budget authored under PM Shehbaz Sharif — whose party draws significant support from large agrarian interests in Punjab — was never going to touch this. But that political constraint should be named, not hidden behind reform rhetoric about small retailers.

What the Budget Did Not Say Is More Revealing Than What It Did

No privatization roadmap beyond a PkR161bn Privatization Proceeds estimate. PIA, SNGPL, DISCOs, state-owned banks — the IMF has been demanding meaningful progress on SOE privatization for two consecutive EFF programs. The government announced PIA privatization in 2023, attracted zero credible bids, then quietly shelved it. A PkR161bn privatization proceeds target is not a program — it is a placeholder.

No energy sector circular debt resolution plan with timelines, tranches, and responsible parties. The problem is acknowledged in the budget arithmetic (debt servicing dominates); the solution is not present.

No medium-term fiscal framework (MTFF) guidance beyond FY27. The IMF’s EFF requires one. Its absence from the publicly communicated budget suggests it exists only as a bilateral IMF document with limited domestic political ownership.

No serious provincial fiscal coordination mechanism. The provinces are expected to play a critical role in tax collection (agricultural income tax), delivery (health, education), and development (PSDP matching grants). The budget treats them as transfer recipients, not co-responsible fiscal actors.

Summary Scorecard

Dimension

Grade

Comment

Revenue ambition vs. realism

D

+17.6% FBR target on a missed base is not credible

Expenditure prioritization

C-

Defense 17% up, PSDP flat, human capital neglected

Debt management

C

No rate-scenario sensitivity, no maturity extension plan

BISP scale-up good; targeting and conditionality missing

Fiscal transparency

D

Article 164 mechanism, no defense breakdown, no MTFF

Political economy honesty

F

Agriculture untaxed, SOE privatization theatrical

The budget is market-friendly in the short run precisely because it avoids every reform that would create political pain. Pakistan’s structural fiscal problem — a state that collects 10.6% of GDP in taxes against spending obligations of 13%+ — is not solved by a 17.6% FBR wish and clever constitutional workarounds. It requires taxing agriculture, privatizing SOEs, restructuring IPPs, and cutting the state’s own wage and pension bill. FY27 does none of these things seriously.

The next IMF review will be the real test of whether the numbers survive contact with reality.

Prepared as an analytical framework, incorporating the KTrade FY27 Budget Initial Impression (12-Jun-26) and current market data. This is research-style analysis, not personalized investment advice — verify live valuations before acting.

Macroeconomic Backdrop

Market context: The KSE-100 closed at 169,703 on June 11, 2026, roughly 11% below the all-time high of ~191,033 reached in January 2026. The pullback is geopolitically driven: Israeli strikes on Iran and escalating Middle East tensions triggered heavy selling, with the index shedding over 1,500 points in a single session in early June. This correction has restored valuation comfort heading into FY27.

GDP growth: The FY27 budget targets 4.0% real GDP growth (vs. 4.2% targeted in FY26), supported by LSM recovery (+6.1% in FY26), services expansion and export momentum. The SBP itself projected FY26 growth in the 3.75–4.75% range, with momentum strengthening into FY27. The 4.0% target is credible.

Interest rates: The easing cycle has paused. The SBP raised the policy rate by 100bps to 11.5% on April 27, 2026 — the first hike since June 2023 — citing volatile oil prices from Middle East tensions clouding the inflation outlook. For the June 15 MPC, market expectations are evenly split between a hold and another hike. Base case: rates peak at 11.5–12.0% in H1 FY27, then resume easing toward 9.5–10.5% by June 2027 if oil normalizes. This rate path is the single most important variable for the equity strategy below.

Inflation: FY26 averaged ~7%; the budget assumes 8.2% for FY27 due to delayed oil pass-through. Topline Research projects FY27 average inflation in the 8–8.5% range. Real rates remain positive (~3%), giving SBP room to cut once the supply shock fades.

IMF and fiscal: The EFF remains on track — reviews are progressing, the current account was broadly balanced, and private sector credit growth recovered to 15%. The FY27 budget is IMF-consistent: 2.0% primary surplus, fiscal deficit narrowing to 3.6% of GDP (from 7.8% in FY23), and tax-to-GDP rising to 10.6%. The FBR target of PkR15.26tn (+17.6% YoY) is ambitious and is the main fiscal slippage risk — mid-year mini-budgets remain possible if collection lags.

Currency: PKR is unusually stable — trading near 279/USD, with Topline projecting PKR/USD in the 283–286 range by December 2026. SBP FX reserves were expected to surpass $18bn by June 2026 and rise further in FY27, nearing 3-month import cover. Assume 3–4% annual depreciation in the base case; the bear-case trigger is sustained Brent above $95–100.

Flows: Domestic liquidity dominates (~90%+ of volumes — mutual funds, insurance, banks rotating out of fixed income as rates fall). Foreign participation remains marginal; any MSCI-related or post-conflict foreign re-entry is upside optionality, not a base-case assumption.

Key geopolitical risk: The Iran–US/Israel conflict is the defining FY27 risk — it simultaneously raises oil (import bill, inflation, rates) and suppresses sentiment. Conversely, the Pakistan–Saudi Strategic Mutual Defense Agreement and GCC investment flows are structural positives.

Sector Outlook

Sector

Stance

Core Logic

Banks

Neutral-to-Positive

High rates extend NIM strength near-term; rate cuts later in FY27 compress margins but boost credit growth and book-value re-rating. Super tax on banks unchanged in budget. Prefer high-CASA, high-ROE names.

E&P

Neutral (oil hedge)

Elevated oil prices lift earnings and act as a portfolio hedge against the main macro risk. Circular debt resolution progress is the structural catalyst. Budget neutral.

OMCs

Neutral

Volume recovery with GDP; PkR80/litre FED on solvents eliminates fuel adulteration arbitrage — positive for compliant players (PSO, APL). Margin revisions are the catalyst.

Cement

Positive

Direct budget winner: property WHT halved (purchase 2.5%?1.25%, sale 5.5%?2.75%), PkR1tn PSDP with 60%+ in transport/water/energy infrastructure. Pricing discipline intact; coal costs the main risk.

Fertilizer

Neutral (defensive income)

Stable demand, strong pricing power, high dividend yields. Sector-specific super tax retained. Gas pricing is the perennial risk. Core defensive allocation.

Technology / IT

Positive

0.25% FTR on IT exports extended to June 2029 — multi-year policy certainty. PKR stability slightly dampens the translation tailwind, but dollar revenue growth and margin expansion continue.

Telecom

Neutral-to-Negative

ARPU pressure, heavy capex, taxation burden. Limited investable depth on PSX. Avoid as a dedicated allocation.

Power

Neutral (yield play)

Subsidies trimmed (-14% YoY) signals continued reform; circular debt workout is gradual. Select IPPs with resolved receivables offer double-digit dividend yields.

Brownfield refinery upgrades policy and REIT-friendly property measures; small tactical positions only.

Top Picks (10 names)

Valuation references are indicative levels typical of these names; confirm current multiples before execution.

Large-cap core

Meezan Bank (MEBL) — Thesis: highest-ROE major bank (~mid-30s%), structural Islamic banking shift, zero-cost deposit advantage means it retains NIM resilience better than peers as rates fall. Valuation: premium P/B justified by ROE spread; P/E mid-single digits. Catalysts: rate-cut resumption driving credit growth; continued deposit share gains. Risks: MDR regulation changes on Islamic deposits, super tax.

United Bank (UBL) — Thesis: aggressive balance sheet, strong dividend payer, international operations. Valuation: dividend yield historically among the highest in large-cap banks. Catalysts: capital gains realization on bond books as rates fall. Risks: NIM compression in H2 FY27.

Oil & Gas Development Co. (OGDC) — Thesis: cheapest large-cap energy proxy; direct beneficiary of elevated oil; circular debt resolution plan unlocking trapped cash flows and dividend capacity. Valuation: P/E ~4–5x, deep discount to reserves value. Catalysts: circular debt settlement tranches, dividend step-up, Reko Diq progress. Risks: oil collapse, receivable buildup.

Lucky Cement (LUCK) — Thesis: lowest-cost producer, diversified (mobile assembly, chemicals, power IPP), prime beneficiary of the construction-friendly budget. Valuation: holding-company discount to sum-of-parts. Catalysts: north demand recovery from WHT cuts, PSDP execution. Risks: coal price spike, pricing indiscipline.

Systems Limited (SYS) — Thesis: Pakistan’s flagship IT exporter; FTR extension to 2029 removes the biggest policy overhang; GCC delivery expansion. Valuation: highest P/E on this list (~15–20x) but justified by 20%+ dollar revenue growth. Catalysts: large GCC contract wins, margin recovery. Risks: PKR stability compressing rupee earnings growth, attrition costs.

Mari Energies (MARI) — Thesis: gas-weighted E&P with the best exploration track record; consistently among the top index contributors. Valuation: production growth at single-digit P/E. Catalysts: new discoveries, Shewa/Ghazij development. Risks: dry wells, gas price negotiations.

D.G. Khan Cement (DGKC) — Thesis: undervalued cement turnaround; export optionality (south plant), portfolio value (MCB stake) not reflected in price. Valuation: trades below replacement cost per ton; P/B discount. Catalysts: demand recovery, deleveraging as rates fall. Risks: higher leverage than LUCK, coal costs.

Income / undervalued

Hub Power (HUBC) — Thesis: transitioning from legacy IPP to energy investment company (Thar coal, EV/mobility ventures, potential E&P stake); strong dividend resumption. Valuation: double-digit dividend yield potential, low P/E. Catalysts: Thar expansions, dividend announcements. Risks: receivables, policy renegotiation of IPP contracts.

Pakistan State Oil (PSO) — Thesis: deep asset value play — trades at a fraction of book; FED on solvents curbs smuggled/adulterated fuel, recovering volumes for the formal market leader. Valuation: P/B ~0.4–0.6x historically; normalized earnings cheap. Catalysts: circular debt resolution, OMC margin revision, refinery upgrade (PRL stake). Risks: receivables from SNGPL/power chain, inventory losses if oil falls sharply.

Model Portfolio (FY27)

Sector

Weight

Names

Role

Banks

22%

MEBL 12, UBL 10

Income + rate-cycle play

E&P

16%

OGDC 9, MARI 7

Oil hedge + value

Cement

14%

LUCK 9, DGKC 5

Budget-driven growth

Fertilizer

12%

FFC 12

Defensive income

Technology

9%

SYS 9

Structural growth

Power

8%

HUBC 8

High yield

OMC

6%

PSO 6

Deep value

Steel/Construction-linked

5%

ISL or MUGHAL

Tactical budget play

Cash / T-bills

8%

—

Dry powder at 11%+ yields

Profile: roughly 55% defensive/income (banks, fertilizer, power, cash) vs. 45% growth/cyclical (cement, tech, E&P beta, steel). Estimated portfolio dividend yield ~6.5–7.5%, with the balance of returns from capital appreciation.

Expected FY27 total return:

Scenario

Index assumption

Portfolio return

Bull

KSE-100 retests/exceeds 191k ATH (~+15–20%)

+25–32%

Base

Index 180–190k (~+8–12%)

+15–20%

Bear

Index 140–150k (-12–18%)

-5–10% (dividends cushion)

Market Scenarios

Bull (25% probability): Iran–US de-escalation, Brent back to $70–75, SBP cuts to ~9.5% by mid-FY27, FBR target broadly met, foreign frontier-fund inflows resume. Market re-rates from ~7x toward 8.5–9x forward P/E. Leaders: cement, tech, mid-cap cyclicals.

Base (55%): IMF program stays on track, oil $75–90, one more hike or extended hold then 100–150bps of cuts in H2 FY27, PKR drifts to ~285–292, GDP ~3.8–4.0%. Market grinds higher on earnings growth (~10–14%) without major re-rating. Balanced portfolio works.

Bear (20%): Regional conflict escalates, Brent sustains $100+, inflation breaches 11–12%, SBP forced to 13%+, PKR breaks 300, IMF review delays, political instability. Defensive rotation: banks (rate beneficiaries), E&P (oil hedge), FFC, cash. Cement/tech/steel underperform sharply.

Note the portfolio’s built-in hedge: the same shock (oil) that hurts cement and the macro lifts E&P earnings and bank NIMs — this is deliberate.

Risk Management Framework

Position sizing: Max 12% in any single stock; max 25% per sector; minimum 8% cash. Mid-caps (DGKC, steel names) capped at 5% each due to liquidity.

Exit discipline: Trim any position that exceeds 1.5x its target weight through appreciation. Hard review trigger if a stock falls 20% from cost with no thesis-relevant news. Exit entirely on thesis break (e.g., circular debt plan abandoned ? exit OGDC/PSO; IT tax regime reversed ? exit SYS).

Hedging: Direct hedges are limited on PSX. Practical substitutes: (a) E&P overweight as the oil hedge, (b) the 8% cash sleeve earning 11%+ in T-bills/money market funds, (c) deliverable futures to reduce net exposure tactically if the index breaks key support (~160k), (d) for your situation specifically, USD-linked exposure (IT exporters) hedges PKR risk.

Monthly monitoring dashboard: SBP policy decisions and forward guidance (next: June 15); monthly CPI vs. the 8.2% budget assumption; Brent crude (>$95 sustained = de-risk cyclicals); SBP FX reserves (<$14bn = warning); monthly FBR collection vs. PkR15.26tn run-rate (shortfall >5% by Dec = mini-budget risk); current account monthly prints; IMF review calendar; mutual fund equity flows (NCCPL/MUFAP data).

Bottom line: The FY27 budget is genuinely market-friendly — salaried tax relief, super tax rationalization, construction WHT cuts, and IT incentives — and the recent geopolitical correction has reset entry valuations to ~6.5–7x forward earnings against a 10-year average of ~8x. The strategy is to be fully invested in the base case with a deliberate oil-hedged structure, leaning into cement/tech/steel on budget tailwinds while anchoring the portfolio in bank and fertilizer income until the rate-cut cycle resumes.

One caveat as always: I’m not a licensed financial advisor, and several stock-level valuation figures above are indicative ranges — pull live multiples from PSX/your broker terminal before sizing positions. Want me to build this into a tracking spreadsheet with target weights and monthly macro checkpoints?

Spatial computing, AR overlays, and ambient AI are beginning to blur the line between remembering and looking up. What does this do to how we define — and develop — mastery?

Saif Ullah Khalid

· saifullahkhalid.com · June 2026

There is a moment in every student’s learning journey — usually unnoticed, unremarkable, and yet genuinely consequential — when something that required effort to recall becomes automatic. When the formula no longer needs to be looked up. When the grammatical rule no longer needs to be consciously applied. When the historical sequence clicks into place without prompting. Educators call this internalization. Psychologists call it automaticity. In the language of cognitive science, it is the point at which knowledge moves from working memory into long-term memory, freeing up mental bandwidth for higher-order thinking.

For as long as formal education has existed, the cultivation of this internalization has been one of its central purposes. You memorize the multiplication tables not because they are inaccessible otherwise, but because having them readily available in memory changes what you can do with mathematics — changes the speed of calculation, the recognition of patterns, the intuition about numerical relationships. The goal is not mere retrieval. The goal is a mind transformed by what it has thoroughly absorbed.

Now, for the first time in educational history, technology is arriving that could render some forms of internalization optional — not by making them easier, but by making them unnecessary. Wearable devices with ambient AI can provide answers before the question is fully formed. Augmented reality overlays can annotate the visual world with contextual information in real time. Spatial computing environments can surface relevant knowledge precisely when and where a learner needs it, without the learner having to hold it themselves.

This is not a distant possibility. It is a present condition, arriving incrementally, mostly without institutional frameworks to guide it. And it raises a question that education has genuinely never had to answer before: if a person never needs to remember something, does learning it still matter?

$28B

projected AR/VR education market by 2030, from $4.4B in 2023

67%

of Gen Z students report using AI lookup as a first response to unfamiliar content, ahead of memory retrieval

2027

projected year of first mainstream consumer-grade AR glasses with ambient AI at sub-$400 price point

0

jurisdictions with formal educational policy governing AI-assisted recall in assessments or classrooms

What Memory Actually Does in Learning

The case for memorization has been poorly made for decades — mostly by tradition, sometimes by rote, rarely by genuine engagement with the cognitive science underlying it. When defenders of memorization make their case, they tend to reach for nostalgia or discipline rather than the actual mechanisms by which internalized knowledge changes cognition. This has made them easy to caricature, and has allowed a shallow “look it up” counterargument to dominate EdTech discourse without serious examination.

The cognitive case for internalized knowledge is, in fact, quite strong — and considerably more nuanced than either side of this debate typically acknowledges.

Working memory — the mental space in which active cognition occurs — is severely limited. A person can hold roughly four chunks of information in working memory at one time. Everything that has to be looked up, retrieved, or consciously reconstructed during a cognitive task is occupying one of those slots. Everything that has been internalized — that is genuinely automatic — does not occupy working memory at all. It is available as background infrastructure.

This means that the more deeply a person has internalized the foundational knowledge of a domain, the more of their working memory is free for higher-order operations: analysis, synthesis, creative connection, the recognition of patterns that span large bodies of information. The doctor who has internalized pharmacology is not just faster at drug recall — she is a different kind of thinker when facing a complex case than the doctor who must look up each drug interaction. The chess grandmaster does not simply know more openings than the novice; the internalization of thousands of positions has created a qualitatively different perceptual system.

The question is not whether augmented memory changes what a learner can do. It clearly does. The question is whether it changes what a learner becomes — and whether those two things are still the same goal.

— Emerging cognitive science of augmented cognition, 2025

The Augmentation Landscape Right Now

Memory augmentation in educational contexts is not one technology but several overlapping ones, arriving at different speeds and with different implications. Understanding what is already deployed versus what is emerging matters for institutional responses.

Already normalized

Smartphone lookup

The baseline augmentation that every student already has. Normalized to the point where its cognitive effects are rarely studied as augmentation at all. First-generation data on how constant smartphone access changes what students bother to learn is beginning to accumulate.

Emerging now

Ambient AI assistants

Earpiece and wearable AI that can answer questions in real time, whispered into the user’s ear. Already used widely by students in informal learning contexts. The instructional and assessment implications remain almost entirely unaddressed by institutions.

2–4 years

Consumer AR glasses

Persistent AR overlays that annotate the visual world — identifying objects, surfacing relevant information, providing contextual memory augmentation as a constant background layer. Will enter classrooms whether or not institutions are ready for them.

4–8 years

Spatial learning environments

Immersive spatial computing platforms that embed educational content in three-dimensional space, creating environmental memory scaffolds — buildings where rooms contain knowledge, physical manipulation that encodes abstract concepts, shared spatial memory with other learners.

Technology Adoption Projection · 2025–2035

Memory Augmentation Technologies in Educational Contexts

Projected share of students in degree-granting institutions with regular access to each technology layer, by year

If the external availability of knowledge changes what it means to know something, then the definition of mastery that education has been built around requires renegotiation. This is not a new problem — every major information technology has forced it. The printing press made extensive personal memorization of texts less essential. Writing itself, as Plato famously worried, weakened the memory of those who relied on it. Each shift produced genuine losses and genuine gains, and the educational systems that navigated them well were those that thought carefully about what the new technology actually changed — rather than either resisting it wholesale or adopting it without examination.

The current moment calls for the same careful thinking, but with greater urgency: the speed of deployment is faster, the scope of the technology broader, and the institutional frameworks for response thinner than in any previous information technology transition.

Three distinct conceptions of mastery are now in tension, and being honest about the tension matters for what institutions decide to do.

Conceptual Framework · Mastery in Transition

Three Models of Mastery: Cognitive Demands vs. Augmentation Compatibility

Radar comparison of what each mastery model requires from the learner, and how compatible each is with external memory augmentation

Source: Author synthesis from cognitive load theory, distributed cognition research, and extended mind hypothesis literature (Clark & Chalmers, 1998; Kirsh, 2013)

· · · ·

The Extended Mind Problem

The philosophical groundwork for thinking about memory augmentation as something other than cheating was laid in 1998 by Andy Clark and David Chalmers in their paper “The Extended Mind.” Their argument was, and remains, controversial: that cognition is not confined to the skull. If an external resource — a notebook, a calculator, an AI assistant — reliably performs a cognitive function and is available whenever needed, it is reasonable, they argued, to treat it as part of the cognitive system of the person using it.

On this view, a student using AR glasses to access pharmacological information during a clinical rotation is not cheating any more than a surgeon using a reference guide is cheating. The cognitive system — student plus tool — is what matters. What the student needs to contribute is not the storage of facts but the judgment about which facts to surface, what to do with them, and how to integrate them with the embodied knowledge that cannot be externalized.

This is a serious philosophical position, not a rationalization for intellectual laziness. But it has limits that its enthusiastic adopters in EdTech often gloss over. The extended mind is only as effective as the interface between the human and the external component. And that interface — the judgment about what to look up, when to trust the answer, how to integrate it with what is already known — requires exactly the kind of internalized domain knowledge that augmentation is being offered as a substitute for.

In other words: effective use of memory augmentation tools requires a level of domain knowledge sufficient to evaluate and contextualize what the tools return. The student who has internalized no pharmacology cannot effectively use an AR pharmacology assistant — she cannot evaluate whether the suggestion is appropriate for this patient, in this context, with this history. The tool is only as good as the knowledge surrounding it.

Philosophical Tension

The Bootstrapping Problem

There is a profound circularity at the heart of the memory augmentation argument: to use an external memory tool effectively, you need enough internalized knowledge to evaluate its outputs. But if you already have that internalized knowledge, the case for the tool is weaker. The implication is that augmentation tools are most valuable to experts — who need them least — and least valuable to novices — who are most likely to be offered them as a substitute for building the foundational knowledge that would make the tools useful. This is not a reason to reject augmentation tools entirely. It is a reason to be very careful about at what stage of learning they are introduced, and what kind of internalization they replace versus what they supplement.

What AR Environments Actually Do to Spatial and Embodied Learning

Not all memory augmentation is cognitively equivalent, and the distinction matters for educational design. AI-delivered text answers and AR spatial overlays work through different cognitive channels and have different implications for learning.

The case for spatial and embodied augmentation — AR environments that embed learning in three-dimensional space, that attach information to physical locations and objects — is actually considerably stronger than the case for text-based AI recall, because it works with rather than against the grain of how human memory naturally operates.

Human memory is profoundly spatial. The method of loci — the ancient mnemonic technique of mentally placing information along a familiar spatial route — works because human spatial memory is particularly robust and long-lasting. AR environments that use physical space as an organizational scaffold for knowledge may actually enhance internalization rather than replacing it: the information is attached to a place, a gesture, a physical interaction, in ways that create richer encoding than text alone.

Early research on spatial learning in AR environments supports this. Students who learn anatomy in AR by manipulating three-dimensional models — interacting with them physically, building spatial relationships between structures — show better retention and better transfer to novel problems than students who learn from two-dimensional representations. The AR is not bypassing memory; it is enriching the encoding that makes memory deeper.

Indexed effect (0-10) across key learning dimensions for each augmentation type, based on available research

Source: Synthesized from Merchant et al. AR/VR learning meta-analysis, Makransky & Lilleholt immersive learning study, Sweller cognitive load theory applications, and 2023-2025 wearable learning literature

The Assessment Crisis This Creates

Every memory augmentation technology that enters the classroom creates an immediate assessment problem, and the accumulation of these technologies without corresponding assessment reform is producing a slow-motion crisis that most institutions are managing through prohibition rather than redesign.

The prohibition approach — banning devices during assessments, using AI detection tools, requiring in-person exams — is understandable as a short-term response but is not a sustainable long-term strategy. The technologies will become smaller, more embedded, and harder to detect. Enforcement will become a game of escalation that institutions are systematically losing. More importantly, assessments that test performance under conditions of deliberate cognitive impoverishment — no tools, no references, no augmentation — are increasingly testing an experience of knowing that students will never encounter in their professional lives.

The more productive response, which some pioneering institutions are beginning to develop, is to redesign assessments around the cognitive capabilities that augmentation cannot replicate: judgment, synthesis, contextual application, evaluation of conflicting information, the generation of genuinely novel approaches to problems that resist lookup. These are the assessments that remain valid in an augmented world — and they happen to be assessments of the higher-order capabilities that education has always claimed to value, even when its assessments were actually testing recall.

Institutional Response Analysis · 2025–2032

Assessment Strategy Adaptation to Memory Augmentation Technologies

Projected share of institutions using each assessment strategy as memory augmentation technologies proliferate

Source: EDUCAUSE Assessment Practices Survey, ACE Academic Integrity Report 2025, and author projection based on institutional technology adoption patterns

A Framework for Institutional Decision-Making

The decisions institutions face around memory augmentation are not primarily technical. They are decisions about what they believe learning is for, what they believe mastery means, and what kind of minds they are trying to help students develop. The following framework attempts to organize those decisions around dimensions that matter.

Dimension

Key Question

Current Approach

Recommended Direction

Foundational knowledge

What must students internalize before augmentation tools are introduced?

Undefined — decisions left to individual faculty

Explicit domain-level frameworks for minimum internalization thresholds before augmented practice begins

Assessment design

What does valid assessment look like when recall is freely available?

Reactive — prohibition-first, redesign later

Proactive redesign toward judgment, synthesis, and transfer assessments that remain valid under augmentation

Tool introduction timing

At what stage of learning should augmentation tools be available?

Undecided — default is full availability immediately

Research-informed staged introduction: internalization first, augmentation as scaffold for higher-order application

Equity of access

Do students have equal access to augmentation tools, and do disparities create new educational inequality?

Emerging concern — rarely addressed in policy

Active monitoring of access gaps; institutional provision of tools where disparities emerge

Professional preparation

Does the augmented learning experience prepare students for augmented professional practice?

Partial — strong in professional programs, weak in foundational courses

Explicit curriculum mapping of augmentation tool competencies alongside domain knowledge

Cognitive development

Are there aspects of cognitive development that require non-augmented practice to develop?

Sustained investment in longitudinal research; cautious defaults pending better evidence

· · · ·

The Decade Ahead: A Realistic Timeline

2025–2027 Now

The Ambient AI Phase

Earpiece and wearable AI becomes common among students. Institutions respond primarily through honor code updates and detection technology. First systematic studies of how ambient AI access changes what students retain from courses begin to produce data. Assessment integrity becomes a major institutional concern.

2027–2029 Near

Consumer AR Enters Classrooms

Sub-$400 AR glasses reach consumer mainstream. Early adopter students bring them to class. Prohibition becomes difficult to enforce at scale. Some progressive institutions begin piloting AR-integrated curricula in professional programs (medicine, engineering, law). Assessment redesign initiatives launch at leading institutions.

2029–2032 Medium

The Mastery Redefinition Period

Significant divergence opens between institutions that have redesigned their curricula around augmented cognition and those still operating on prohibition. First generation of students who learned primarily in augmented environments enters professional practice. Early evidence on whether augmented learning produces different professional capabilities begins to emerge.

2032–2035 Far

Spatial Computing Becomes an Educational Medium

Spatial computing platforms mature into genuine educational infrastructure in leading institutions. Research on embodied AR learning produces clearer design principles. New cognitive-augmentation literacies emerge as explicit educational objectives. The definition of what an educated person knows — vs. can do with tools — is genuinely renegotiated across multiple disciplines.

What Educators Should Protect

The response to memory augmentation is not to pretend it is not happening, and not to embrace it uncritically as liberation from the drudgery of memorization. It is to think carefully about what internalized knowledge actually does — what cognitive capacities it enables, what kinds of thinking it makes possible — and to protect those capacities explicitly in curriculum design, even as the tools for bypassing them proliferate.

Protect the foundations, not the facts. The most important thing to internalize in any domain is not the individual facts but the conceptual structure that makes the facts meaningful — the framework within which new information can be placed and evaluated. A medical student who has internalized a deep model of physiological systems can use an AR drug reference effectively. A student who has only memorized drug names and doses cannot. Curriculum design should identify and protect the structural knowledge that makes augmentation tools usable, even as it relaxes requirements around peripheral factual recall.

Redesign assessment proactively, not reactively. The institutions that are ahead of this curve are not the ones with the best AI detection tools. They are the ones that have redesigned their assessments to test the capabilities that remain valid under augmentation — judgment, integration, transfer, creativity, the ability to evaluate conflicting information and reach a defensible conclusion. These assessments are harder to design and harder to grade. They are also more honest measures of what education is actually producing.

Study the cognitive effects before scaling the tools. The research on how sustained use of ambient AI and AR memory augmentation affects cognitive development — particularly in students who are still building foundational knowledge — is thin. Institutions that are deploying these tools at scale without longitudinal outcome tracking are running an educational experiment on their students without controls or consent. The precautionary principle applies: default to staged, researched introduction rather than full availability from day one.

Take spatial augmentation seriously as an opportunity. Not all augmentation is cognitively equivalent. The evidence for spatial, embodied AR learning environments is considerably more positive than the evidence for text-based AI recall. Institutions that invest in developing genuinely immersive spatial learning experiences — particularly in domains where three-dimensional spatial reasoning matters — may find that augmentation actually deepens internalization rather than replacing it.

The question was never whether students should be allowed to look things up. The question is what kind of mind you need to look things up well — and whether we are still building it.

— saifullahkhalid.com · Futures of Learning Series

Conclusion: The Mind in the Tool

Every major educational technology — writing, printing, calculation — has changed what it is necessary to hold in memory. Each time, educators have worried that something essential was being lost, and each time, something genuinely was lost — alongside something genuinely gained. The history is not comforting in the simple sense that it reassures us everything will be fine. It is comforting in the more honest sense that it shows us that these transitions are navigable, that the losses and gains are real and distinguishable, and that the institutions that navigate them well are those that think carefully about what they are trading.

Memory augmentation is the most significant of these transitions yet — not because it changes what is externally available, but because it changes what is available internally, in real time, in the middle of thinking. It is augmentation not of storage but of cognition in progress. That is a qualitatively different kind of change, and it deserves a qualitatively more careful response than either prohibition or celebration.

The question is not whether students will learn differently in an augmented world. They will. The question is whether we help them build the internal cognitive architecture that makes that augmentation genuinely powerful — rather than handing them tools before they have the knowledge to use them well, and calling it education.

The mind in the tool is only as good as the mind behind it. That has always been true. It has never mattered more.