|

Getting your Trinity Audio player ready...

|

This is a structural critique, not a political one. The budget has genuine positives, but several decisions are either analytically weak, fiscally reckless, internally contradictory, or represent missed reform opportunities that Pakistan may not get again for years.

- The Revenue Target Is a Fantasy Dressed as a Plan

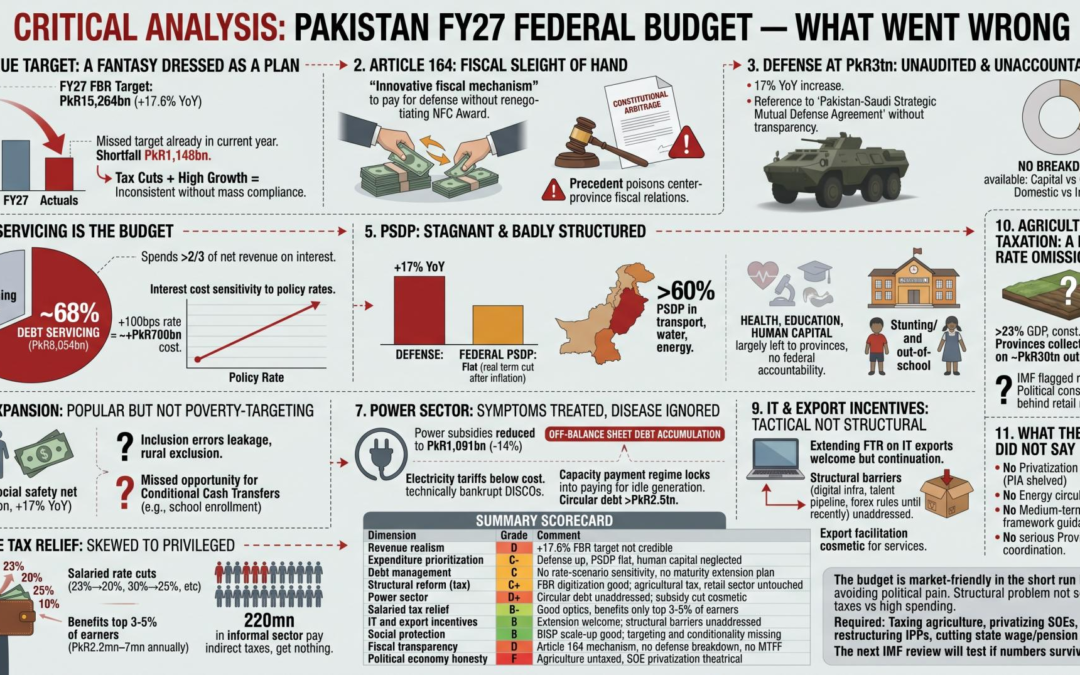

The FBR target of PkR15,264bn (+17.6% YoY) is the budget’s most dangerous number.

The current year’s revised estimate already missed the original PkR14,131bn target, coming in at PkR12,983bn — a shortfall of PkR1,148bn. Pakistan’s FBR has never delivered 17.6% growth on a realistic base in a single year through genuine broadening of the tax net. Every time they’ve come close, it was driven by inflation (more rupees chasing same goods) or one-off measures, not structural reform.

Now they are simultaneously cutting super tax, slashing WHT on property, reducing IT and export taxes, and abolishing multiple levies — all of which reduce the tax take — while expecting 17.6% revenue growth. These two things cannot coexist without either massive new compliance enforcement (which has never materialized in Pakistan’s history) or a mid-year mini-budget.

What should have been done: Set a realistic 10–12% growth target and front-load the structural reforms to broaden the base — agricultural income tax (a constitutional provincial subject but politically avoidable), taxing the retail and wholesale trade sector properly (not a flat 1% regime that formalizes under-declaration), and moving the documented-to-undocumented economy ratio from the current ~40% toward 60% over three years with binding milestones. The FBR Reform section (National Faceless Centre, double-blind audit) is genuinely good — but it’s a medium-term intervention being sold as an FY27 revenue contributor, which it is not.

- The Article 164 Mechanism Is Fiscal Sleight of Hand

The budget introduces a “cooperative federalism” mechanism under Article 164 — incremental FBR collections between PkR13,350bn and PkR15,264bn flow back to the Federation as strategic grants to finance defense. The document calls it “an innovative fiscal mechanism.”

What it actually is: a method to pay for a PkR3tn defense budget without formally renegotiating the 7th NFC Award, so provincial shares remain nominally intact while the Federation reroutes the incremental collection. This is not fiscal innovation — it is constitutional arbitrage. It sets a precedent that the NFC Award is circumventable by executive design, which will poison center-province fiscal relations for years. Khyber Pakhtunkhwa and Sindh in particular have strong incentives to challenge this legally, and they should.

More importantly, the mechanism only works if FBR collects the incremental PkR1,914bn (from PkR13,350bn to PkR15,264bn). Given the above analysis on revenue targets, this incremental amount is almost certainly not going to be collected, meaning the Federation either borrows to fund defense or cuts civilian spending mid-year.

What should have been done: A transparent renegotiation of the NFC Award to reflect contemporary expenditure realities — particularly on defense and federal development — rather than engineering workarounds that undermine the constitutional architecture.

- Defense at PkR3tn Is Unaudited and Unaccountable

Defense spending rose 17% YoY to PkR3tn, justified by “post-Operation Bunyan-ul-Marsous realities and the Pakistan-Saudi Strategic Mutual Defense Agreement.” There is no breakdown of this PkR3tn in the public budget documents. Capital vs. current. Personnel vs. procurement. Domestic vs. import-dependent.

For context, defense at PkR3tn now represents approximately 2.09% of nominal GDP (PkR143.6tn) and is larger than the entire Federal PSDP (PkR1tn). Pakistan spends more on military than on development. This is not abnormal by South Asian standards, but it is unsustainable at this deficit level.

The more pressing issue: the Pakistan-Saudi Strategic Mutual Defense Agreement is referenced as fiscal justification for a 17% surge in defense spending, but the terms of this agreement have not been placed before parliament. Tying permanent expenditure increases to undisclosed bilateral commitments is a governance failure.

What should have been done: Even a high-level defense budget breakdown (capital vs. recurrent; percentage domestically produced vs. imported) would allow economists and parliament to assess the import-bill impact and the domestic multiplier effect. Pakistan’s defense imports consume scarce foreign exchange and generate minimal domestic value-add. Without visibility, we cannot optimize.

- Debt Servicing Is the Budget — Everything Else Is Residual

Debt servicing at PkR8,054bn represents 43% of total expenditure and 68% of net revenue receipts. Pakistan is spending more than two-thirds of every rupee it collects in net revenues on interest payments alone. This ratio has improved from its FY25 peak (where debt servicing briefly exceeded net revenue receipts entirely), but it remains structurally crippling.

The budget treats the decline in debt servicing as a success story — and technically, the drop from PkR8,206bn (budgeted FY26) to PkR8,054bn (FY27 budget) is progress driven by falling rates. But the FY27 budget simultaneously assumes 11.5% policy rate (post the April hike) with possible further tightening in June, which means T-Bill rollovers and PIB auctions through FY27 will be priced at rates higher than assumed when this debt-servicing estimate was computed.

If the June 15 MPC delivers another 50–100bps hike (which 49% of surveyed analysts expect), the PkR8,054bn estimate is immediately undercooked. Every 100bps increase on a ~PkR70tn domestic debt stock adds roughly PkR700bn in annual interest cost — the entire BISP budget wiped out in one rate decision.

What should have been done: The budget needed a sensitivity table showing debt servicing under 11.5%, 12%, and 12.5% policy rate scenarios. It also needed an aggressive domestic debt maturity extension program — locking in current rates by issuing long-duration Sukuks and PIBs before any further hikes — rather than continuing to rely on short-duration T-Bill rollovers that amplify rate exposure.

- The PSDP Is Stagnant and Badly Structured

Federal PSDP is maintained at PkR1,000bn — same as FY26’s budgeted figure. At face value, this looks like continuity. In real terms, it is a cut (inflation of 8.2% implies PkR918bn in real PkR26 terms). Against a PkR18.8tn expenditure budget, the development allocation is 5.3% of total spending.

The structural problem: over 60% of PSDP is in transport, water, and energy. These are legitimate priority sectors, but this concentration means health, education, and human capital development — the actual drivers of long-run productivity — are largely left to provinces through the NFC transfer, with no federal accountability mechanism for outcomes.

Pakistan’s human development indicators are catastrophic for a lower-middle income country. ASER Pakistan consistently shows over 22 million out-of-school children. Stunting affects ~40% of children under 5. These are not solvable through transport infrastructure alone. A budget that raises defense by 17% and holds PSDP flat is implicitly choosing short-run security over long-run productivity.

The other structural flaw: PSDP execution has averaged roughly 70–80% of allocation for years. Budgeting PkR1,000bn when you know PkR700–750bn will actually flow is poor public financial management. Either budget what you can execute, or fix the execution machine — the budget does neither.

What should have been done: Reduce PSDP headline to PkR800bn with a realistic execution plan, allocate 20–25% to human capital (nutrition, teacher training, primary health), and link remaining disbursements to measurable deliverables rather than phased allocations that stall in bureaucracy.

- BISP Expansion Is Politically Popular but Not Poverty-Targeting

BISP allocation at PkR838bn (+17% YoY) is the largest social safety net in Pakistan’s history, and this is a genuine achievement. However, several structural critiques apply:

First, 17% growth in BISP spending while real GDP grows at 4% means BISP is growing 4x faster than the economy. This is only sustainable if it is being financed by genuine revenue growth — which we established above is unlikely.

Second, the BISP beneficiary database has well-documented inclusion errors. Multiple audits and BISP’s own data show significant leakage to non-poor households and exclusion of genuinely poor households, particularly in rural Balochistan and FATA. Throwing 17% more money into a targeting system that hasn’t been rigorously re-validated is wasteful.

Third, BISP is unconditional cash. There is strong international evidence for conditional cash transfers — tying payments to school enrollment, vaccination, or maternal health checkups — generating better development outcomes per rupee spent. Pakistan’s own evidence base from pilot programs supports this. The budget missed an opportunity to shift BISP toward conditionality at scale.

- Power Sector: Symptoms Treated, Disease Ignored

Power subsidies are reduced to PkR1,091bn (-14% YoY). This looks like fiscal discipline. It isn’t — it’s a reduction in one line item while the circular debt stock continues accumulating off-balance-sheet in the power sector’s borrowings from commercial banks.

The structural problem is that electricity tariffs remain well below cost-recovery for residential consumers, the distribution companies (DISCOs) are technically bankrupt loss-making SOEs hemorrhaging PkR400–600bn per year in T&D losses and theft, and the capacity payment regime (the result of take-or-pay IPP contracts signed in 2015 and 2021) locks Pakistan into paying for idle generation capacity regardless of demand.

Nothing in the FY27 budget addresses the root cause: either restructure the IPP contracts (which the government started doing in FY25 but quietly stalled), aggressively privatize/corporatize DISCOs with a hard political mandate, or move to cost-reflective tariffs with targeted subsidy for the lowest consumption bracket only.

The budget’s power sector answer is: reduce the subsidy line item and hope the problem migrates off the headline budget. The circular debt stock has already crossed PkR2.5tn. This is a crisis deferred, not resolved.

- The Income Tax Relief Is Skewed to the Already-Privileged

The salaried class tax relief — rate reductions from 23%?20%, 30%?25%, 35%?29% and 35%?32% for incomes between PkR2.2mn and PkR7mn annually — is being presented as middle-class relief. These are actually incomes between roughly $7,800 and $25,000 per year at current exchange rates. The people earning PkR2.2mn–7mn annually are in the top 3–5% of Pakistan’s income distribution.

Pakistan’s total documented salaried taxpayer base is approximately 2.5–3 million people in a country of 257 million. The budget reduces the tax burden on these 2.5 million people while doing essentially nothing for the 220 million in the informal sector who pay indirect taxes (GST, FED) on every item they buy but have no formal income tax obligation because they are undocumented.

The abolition of the income surcharge is the same story: this was charged only on salaried incomes above PkR10mn — i.e., the top fraction of the top 5%. Abolishing it costs the government revenue and delivers a benefit entirely to the richest documented earners. Framing this as salaried class relief is a messaging choice, not an economic characterization.

What should have been done: the marginal rate cuts should have focused on the PkR600,000–PkR2.2mn annual income bracket (annual salary of PkR50,000–183,000/month), which represents the genuinely vulnerable lower-middle documented class. The upper bracket already benefits from cost-of-living perks, car allowances, medical, and bonus structures that are effectively tax-free.

- The IT and Export Incentives Are Tactical, Not Structural

Extending the 0.25% FTR on IT exports to June 2029 is welcome, but it is a continuation of a regime due to expire — not an expansion. Pakistan’s IT exports were approximately $3.2bn in FY25, against India’s $254bn and Egypt’s $6bn (a country with a smaller tech talent base). The gap is not primarily because of tax rates. It is because of regulatory friction (forex repatriation rules until recently), inadequate digital infrastructure outside Karachi/Lahore/Islamabad, visa difficulty for foreign clients visiting Pakistan, and the talent pipeline bottleneck.

None of these structural barriers are addressed in the budget. The export facilitation measures (EFS markup at 4.5%, 9?18 month extension) are useful for manufacturing exporters but cosmetic for services exporters.

The reduction in WHT on international card transactions from 5% to 0.5% is overdue and genuinely beneficial for freelancers and IT firms, and this is one of the budget’s cleaner wins. However, even this measure was only necessitated by the fact that Pakistan drove significant dollar transactions underground through an indefensible 5% levy in the first place.

- Agricultural Taxation: A Deliberate Omission

Agriculture contributes roughly 23% of GDP and is constitutionally taxed at the provincial level. Provinces consistently fail to collect meaningful agricultural income tax — the total collected across all four provinces is typically under PkR10bn annually on a sector generating PkR30+ trillion in output. This is the single largest source of tax expenditure in Pakistan’s fiscal system, and it is entirely absent from the FY27 federal budget.

The IMF has flagged agricultural income taxation repeatedly. The FBR Reform section is eloquent about digital audit trails and faceless tax centres. None of it touches the feudal land-owning class that structurally dominates parliament and has blocked this reform for 75 years. A budget authored under PM Shehbaz Sharif — whose party draws significant support from large agrarian interests in Punjab — was never going to touch this. But that political constraint should be named, not hidden behind reform rhetoric about small retailers.

- What the Budget Did Not Say Is More Revealing Than What It Did

No privatization roadmap beyond a PkR161bn Privatization Proceeds estimate. PIA, SNGPL, DISCOs, state-owned banks — the IMF has been demanding meaningful progress on SOE privatization for two consecutive EFF programs. The government announced PIA privatization in 2023, attracted zero credible bids, then quietly shelved it. A PkR161bn privatization proceeds target is not a program — it is a placeholder.

No energy sector circular debt resolution plan with timelines, tranches, and responsible parties. The problem is acknowledged in the budget arithmetic (debt servicing dominates); the solution is not present.

No medium-term fiscal framework (MTFF) guidance beyond FY27. The IMF’s EFF requires one. Its absence from the publicly communicated budget suggests it exists only as a bilateral IMF document with limited domestic political ownership.

No serious provincial fiscal coordination mechanism. The provinces are expected to play a critical role in tax collection (agricultural income tax), delivery (health, education), and development (PSDP matching grants). The budget treats them as transfer recipients, not co-responsible fiscal actors.

Summary Scorecard

| Dimension | Grade | Comment |

| Revenue ambition vs. realism | D | +17.6% FBR target on a missed base is not credible |

| Expenditure prioritization | C- | Defense 17% up, PSDP flat, human capital neglected |

| Debt management | C | No rate-scenario sensitivity, no maturity extension plan |

| Structural reform (tax) | C+ | FBR digitization good; agricultural tax, retail sector untouched |

| Power sector | D+ | Circular debt unaddressed; subsidy cut cosmetic |

| Salaried tax relief | B- | Good optics, benefits only top 3-5% of earners |

| IT and export incentives | B | Extension welcome; structural barriers unaddressed |

| Social protection | B | BISP scale-up good; targeting and conditionality missing |

| Fiscal transparency | D | Article 164 mechanism, no defense breakdown, no MTFF |

| Political economy honesty | F | Agriculture untaxed, SOE privatization theatrical |

The budget is market-friendly in the short run precisely because it avoids every reform that would create political pain. Pakistan’s structural fiscal problem — a state that collects 10.6% of GDP in taxes against spending obligations of 13%+ — is not solved by a 17.6% FBR wish and clever constitutional workarounds. It requires taxing agriculture, privatizing SOEs, restructuring IPPs, and cutting the state’s own wage and pension bill. FY27 does none of these things seriously.

The next IMF review will be the real test of whether the numbers survive contact with reality.